Budgeting: A boring necessity.

During 2021 I realised that I needed to get control of my finances by using a budget to track my monthly expenses, debts and savings goals.

Budgeting is not the most exciting of subjects to cover but in order to gain control of your finances it is an important issue to review.

Why budget?

I have to admit that when lockdown hit at the beginning of the covid pandemic I was very lucky; in part, because thanks to furlough in the UK the staff at the company I worked for were able to be kept on and secondly because I was still able to work from home. It wasn't long however before debts crept up as we tried to keep a toddler entertained and for one reason or another various household items chose to end their lifecycle at the same time such as the vacuum cleaner, pressure washer, washing machine and tv. During 2021 I realised that I needed to get control of my finances by organising a budget so I could track my monthly expenses, debts and savings goals.

Where to start?

The easiest place to start was to set up a spreadsheet and put my net income at the top. This is simple as it is the amount that enters my bank account each month after tax, NI and pension. I then went through our joint account to determine the main expenses that were a regular monthly payment. Starting with the highest (mortgage) I worked through our statement until all payments were listed in order down to Netflix at the bottom. I could then work out which parts I could try and reduce the cost of such as our Virgin Media account and which ones I could remove if there were an emergency in the future that required some cost trimming such as Netflix. It also allowed me to work out a monthly food budget which was the amount most likely to change depending on the products that needed buying.

Next, I worked out what personal debts I had coming out of my current account such as my car lease, car insurance etc. These could be added to my monthly payments list allowing me to subtract them from my net income. Leftover money could then be distributed towards an emergency fund and savings. I may look into other methods such as paying myself first but for now, my primary method would at least get my budget on track.

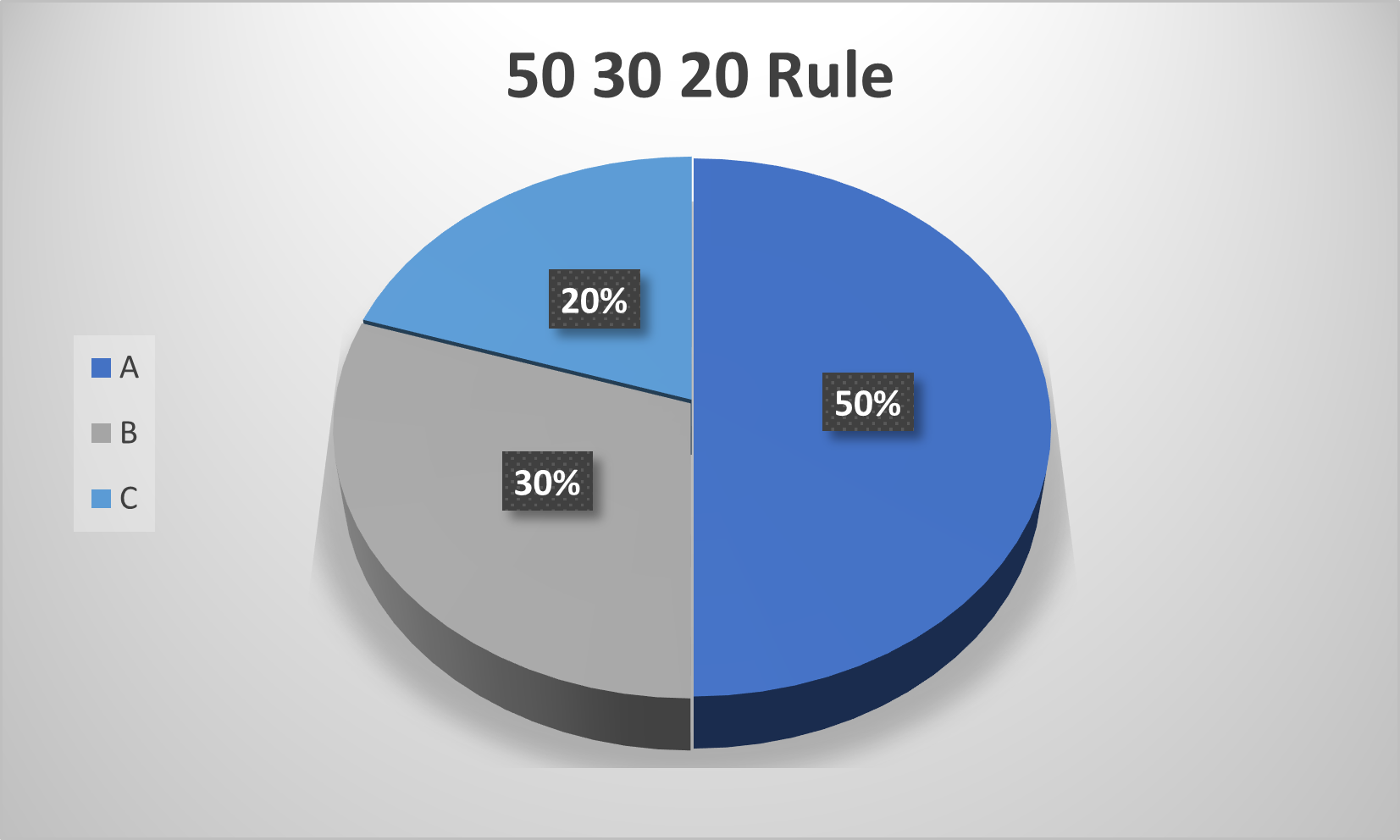

The 50, 30, 20 rule.

The 50,30,20 rule was popularised by US Democrat Senator Elizabeth Warren in her 2005 book, “All Your Worth: The Ultimate Lifetime Money Plan” and is a way of budgeting that splits the budget into three distinct categories:

- Needs - 50% of your net income should cover the costs for your regular monthly payments such as mortgage/rent, utilities, minimum loan payments and your basic groceries.

- Wants - 30% can go towards items that you want including groceries that are not essential, subs such as Amazon Prime, gym membership, dining out etc.

- Savings - 20% can either go to reducing loans by overpaying on the minimum amount or towards savings such as a JISA, ISA or Pension etc.

So as an example if you have a net income of £2,000 a month £1,000 would go towards 'Needs', £600 towards 'Wants' and £400 into 'Savings'. If you find yourself overspending on 'Wants' then look to reduce them so that you put more towards the 'Savings' goal. To fulfil my budgeting goals I took the basics from this way of budgeting and tweaked it to fit my circumstances.

Are there other budgeting options?

There are other budgeting options available such as the envelope (cash-based) and zero-based budgeting methods. I didn't feel like these would be a good fit for me so they won't be covered in great detail. The envelope method involves adding cash to separate envelopes once the main monthly payments have been made so you cannot overspend as you only have a limited amount of money in each category. Zero-based budgeting is a method which allocates the entire monthly budget to expenses, savings and debt payments so you know exactly where all of your money is going to the last penny which is a stricter version of the 50/30/20 method.

Will I change the way I budget in the future?

Just because the way you budgeted at one point in your life was helpful doesn't mean you have to continue budgeting in the same way. I will review my budgeting method once I have read, summarised and reviewed 'The Richest Man in Babylon' which promotes the 'pay yourself first' way of reverse budgeting. The next item on my personal finance agenda though is to look at building an emergency fund.

Comments ()